The healthcare industry in Brazil – main characteristics and opportunities for Finnish companies

This report intends to provide useful information and analysis for Finnish companies interested in accessing the Brazilian healthcare sector. The first section of the report will briefly present information on the main characteristics of the healthcare sector in Brazil, highlighting major players and trends. Next, the report will discuss the recent dynamics of the Brazilian population, an aspect with great influence on the healthcare market, particularly due to the increasing share of elderly people in the population. The following section will focus on health expenditure, and it will present information on the relevance of the Brazilian healthcare market on the world stage and on the profile of expenditure in Brazil vis-à-vis other major countries in the sector. The last two sections of the report will analyse foreign trade and investments and major players operating in the market. The goal of these sections will be providing information on goods demanded by the market, the degree of foreign interest in it and the profile of companies demanding health goods and products. At last, the study will present the main conclusion and a summary of opportunities.

KEY TAKEAWAYS

- Brazil’s healthcare sector is one of the largest in the world.

- Important aspects affecting the market: demographic transition and ageing population.

- Another important aspect to be considered is the increasing degree of digitalisation in the sector.

- Both the public and private sectors are massive players in the Brazilian healthcare sector. Brazil is a relevant importer of pharmaceuticals and medical supplies and equipment.

- Large domestic players and subsidiaries of leading multinational companies operate in the sector.

MAIN CHARACTERISTICS OF THE HEALTHCARE SECTOR IN BRAZIL

In the last decades, Brazil has been adopting policies directed at achieving universal health coverage in the country. Brazil’s current constitution, adopted in 1988, established the Unified Health System (Sistema Único de Saúde – SUS), which grants access to health services to the entire population of the country. The SUS is financed by taxes and the services offered by the system are free of charge.

The SUS operates under a decentralised governance and all government levels in Brazil participate in its administration. At the federal level, the Ministry of Health is responsible for coordinating the system and for monitoring and evaluating services and policies. The health secretariats of the state governments are involved in the regional governance of the system and in strategic programmes and specialised services. Municipal governments are responsible for delivering health services and participating in the co-financing of programmes. The public health system is complemented by the private sector, which is sizeable and plays a relevant role in Brazil.

Two regulatory agencies operate in the health sector in Brazil, the Brazilian Health Regulatory Agency (Anvisa) and the National Agency of Supplementary Health (ANS). Anvisa is responsible for sanitary control of goods subject to health regulation, including pharmaceuticals, and ANS is responsible for regulating private companies offering health insurance in Brazil.

In order to supply the public health system, the government of Brazil demands massive quantities of products, being the main purchaser of healthcare products in the country. In general, foreign companies established in the country are allowed to participate in the bids organised by the government to procure healthcare supplies. Foreign companies operating in Brazil may also take part in Partnerships for Productive Development(PDP, In Portuguese, Parcerias para o Desenvolvimento Produtivo), a mechanism which allows private companies to partner with government institutions to supply the public health system for periods of up to 5 years through contracts which result in technology transfer at the end of the period.

In terms of digitalisation, Brazil has been adopting a good number of measures to allow technology to be adopted more intensively in healthcare. One of the most relevant initiatives is the Brazilian National Digital Health Strategy (RNDS), a plan to be implemented for the period 2020-2028 aiming to establish a network that will connect data and public and private entities involved in healthcare. Other relevant measures related to digitalisation include pieces of legislation adopted last year to regulate telehealth and the use of software as a medical device (SaMD). With the Covid-19 pandemic, telehealth became more popular in Brazil and this modality is considered to be a potential tool to augment the penetration of health services by the public system in remote areas of the country.

It is worth mentioning that in 2015, Brazil passed a law allowing foreign companies to provide health services in the country. The new legislation resulted in greater interest by overseas players in the sector and an increase in inflows of foreign investment in health into Brazil. Also related to market access, another important instrument published in 2022 is an Anvisa resolution which regulates optimised procedures for the acceptance of analyses made by foreign authorities in the context of sanitary approval processes.

The next sections of the report will analyse data and trends shaping the healthcare sector in Brazil. The analysis intends to provide useful information which can help Finnish companies understand the main characteristics about the sector in Brazil and identify business opportunities in the country.

RECENT DYNAMICS OF THE BRAZILIAN POPULATION

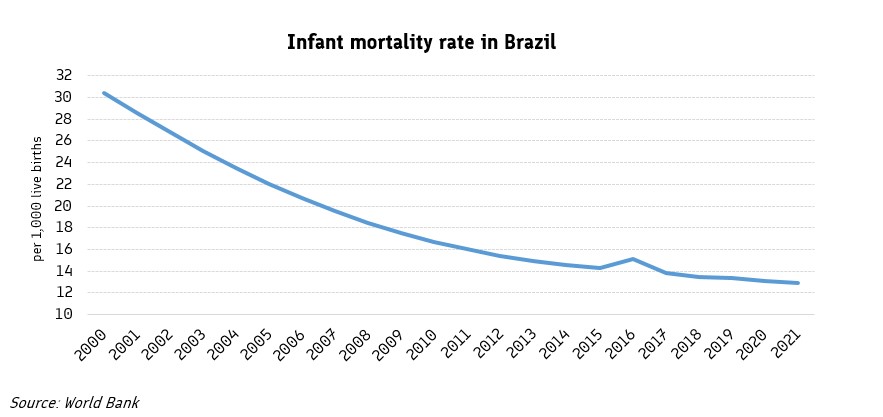

One of the main factors affecting the healthcare sector in Brazil is the profound demographic transition the country is currently experiencing. Advances in healthcare in Brazil have been leading to significant improvements in life expectancy and infant mortality indicators. Life expectancy in Brazil has been increasing in the last years and currently people are expected to live on average until 77 years of age, more than 2 years longer in relation to a decade ago. Also, infant mortality has been decreasing sharply. While in 2000 the infant mortality rate was more than 30 per 1,000 live births, in 2021 the indicator reached 12.9, following a steep downward trend during the period. The next two charts present information on life expectancy and infant mortality in Brazil in recent years.

Concerning causes of death in Brazil, the main factors responsible for deceases are cardiovascular diseases, cancer, respiratory conditions and injuries (intentional and unintentional). Most of the main death causes in the country are associated to an ageing population and a highly urbanised society (in Brazil, 85% of inhabitants live in urban areas). Brazil could certainly be an important market in the present and in the future for companies offering solutions directed at these causes. The following chart presents information on the ten main causes of death in Brazil.

PROFILE OF THE HEALTHCARE EXPENDITURE IN BRAZIL

As one of the largest countries in the world in terms of population and gross domestic product (GDP), Brazil is also a sizeable market in the healthcare sector. The country is the world’s eighth largest country in health expenditure and the only Latin American country among the top ten countries in the indicator. In the Latin American context, Brazil presents a strong relevance in the market, with a health expenditure level over two times higher in relation to the second largest country, Mexico. The next two charts present information on the largest countries in health expenditure in the world and in Latin America, respectively.

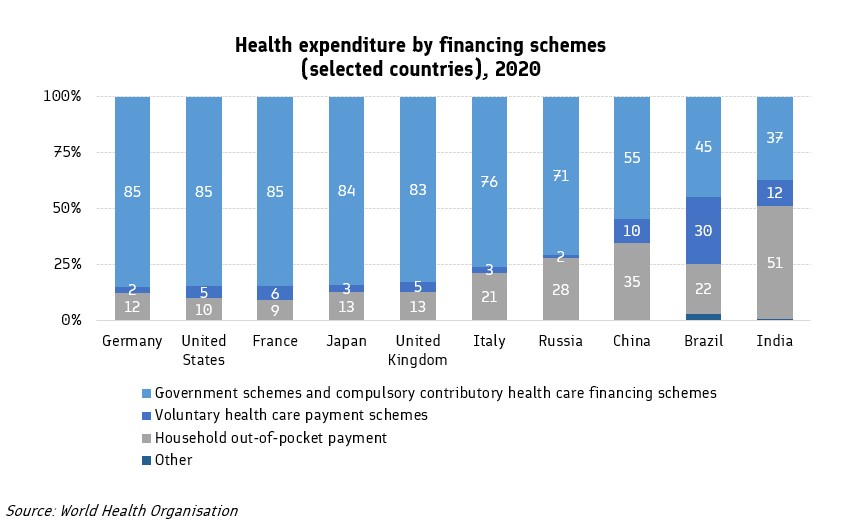

Another important characteristic of Brazil’s healthcare sector is the high participation of the private sector in overall expenditures, although Brazilians have universal coverage through the public system. As shown in the chart below, in Brazil the public share of overall spending is low in comparison to the levels registered by the major healthcare markets in the world.

In terms of healthcare services, a substantial share of Brazilians are covered by private schemes which are commonly offered as benefits by employers. As shown in the following chart, Brazil is the country with the highest share of voluntary healthcare payments in relation to all financing schemes among the largest markets in the world, with a share of 30%. That figure is significantly higher in relation to both developed and developing countries, considering the largest economies in the world.

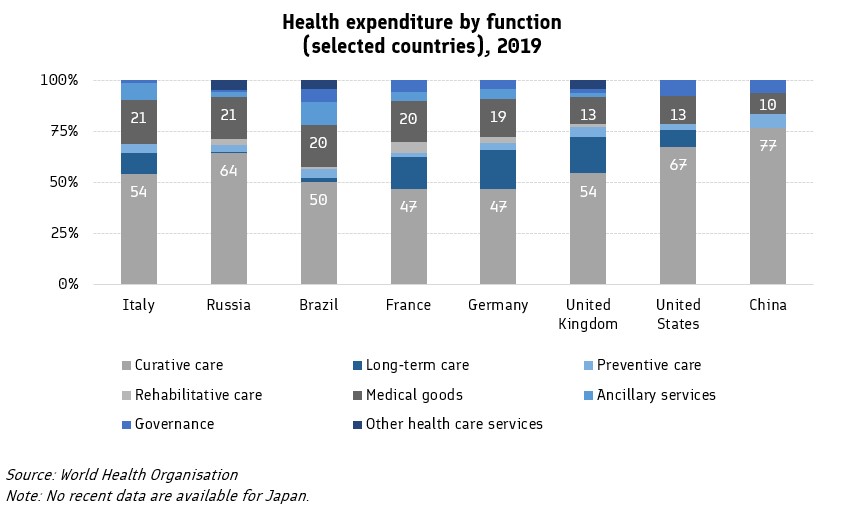

Moreover, out-of-pocket expenses account for a significant share of health expenditure in Brazil (22%, according to the chart above), and the purchase of pharmaceuticals is a relevant component of this type of expense. As the public system accounts for a small proportion of pharmaceutical spending in Brazil (9%, according to a report published by the Organisation for Economic Co-operation and Development), occasionally the purchase of medicines in Brazil is made by individuals in pharmacies with their own resources. The next chart presents additional information that indicates the relevance of pharmaceuticals in overall medical expenses in Brazil. In the country, medical goods (which include pharmaceuticals) account for 20% of health expenditure by function, a high proportion vis-à-vis major healthcare markets in the world.

Finally, it worth noting the importance of generics in the Brazilian pharmaceuticals market. Considering the weight of pharmaceuticals in health expenses in Brazil, the country is a large market for generics, as this type of medicine is offered at lower prices to consumers. Even if compared to other Latin American countries, the share of generics in the retail pharmaceutical market is considerably high in Brazil, at a level close to 70%. The chart below presents information on the indicator for selected Latin American countries.

FOREIGN TRADE AND INVESTMENTS IN HEALTHCARE IN BRAZIL

Brazil is an important market for healthcare products produced overseas. In the last ten years, annual imports of healthcare products by the country stood for most years between US$ 12 billion and US$ 15 billion (a one-off peak was registered in 2021, possibly as a consequence of the Covid-19 pandemic).

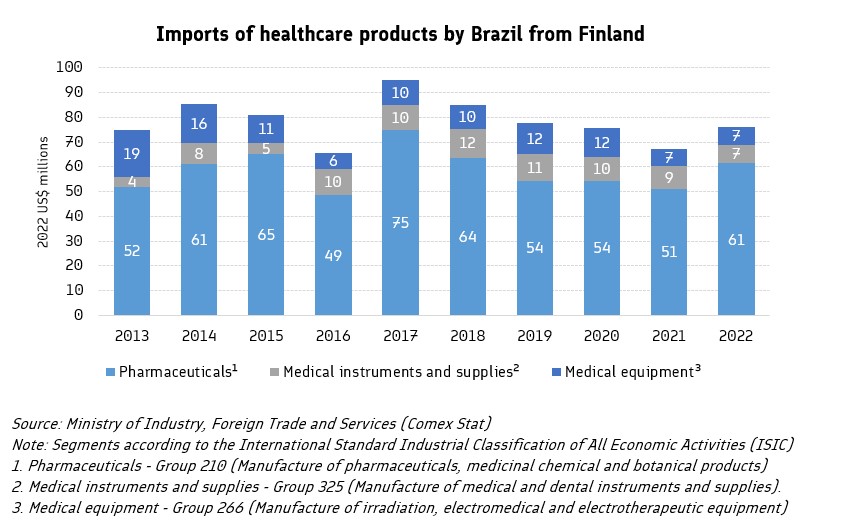

Although pharmaceuticals account for the bulk of imports (74% on average between 2013 and 2022), medical equipment and supplies have also presented sizeable volumes. Annual imports of medical supplies averaged US$ 2.5 billion in the last years and for medical equipment the average was US$ 1.1 billion.

The profile of Brazilian imports of healthcare products from Finland follows a similar pattern in relation to the profile of imports from the world as a whole. Nevertheless, in the case of Finnish imports, medical equipment accounts for a larger share of total imports. The next two charts present information on annual imports by Brazil of health products from the world and from Finland, respectively.

Regarding foreign direct investment (FDI) in health in Brazil, when it comes to pharmaceuticals the stock of investments followed a downward trend between 2014 and 2020. Among the reasons for the decline are the closing of factories by foreign pharmaceuticals companies and the selling of lower-value medicine brands (including generics) to domestic players. Both factors are associated to a strategy adopted by foreign companies of concentrating in the production of more complex medicines and moving production of these products to locations which present higher competitiveness in this segment. For instance, in 2019 Eli Lilly and Roche announced the closure of factories in Brazil. Concerning the selling of medicine brands, both Boehringer Ingelheim and Takeda sold assets to Brazilian pharma company Hypera, for example.

The chart below shows the trajectory of FDI stocks in the Brazilian pharmaceuticals sector in the last ten years. Also in this case the Covid-19 pandemic could have been the factor behind the sharp rise in the indicator in 2021.

As regards foreign investments in health services, the stock of FDI in the segment rose sharply after the legislation change opening the sector to foreign capital in 2015. Examples of foreign companies investing in health services since then include the acquisition of shares of Oncoclínicas by Goldman Sachs (between 2015 and 2019) and the acquisition by Advent International of 13% of Fleury’s equity in 2015 (later sold in 2017). The following chart shows the trajectory of FDI stocks in health services in the last ten years.

MAJOR PLAYERS IN THE HEALTHCARE SECTOR IN BRAZIL

Large domestic players and foreign enterprises operate in the healthcare sector in Brazil, and these companies play an important role as buyers and sellers of health goods and services in the country.

When it comes to pharmaceuticals, major players are subsidiaries of large multinational companies and Brazilian players that have been expanding significantly in recent years and that focus mainly on the production of over-the-counter medicines and generics.

In relation to health services providers, the most relevant players are companies that operate hospitals and clinics and large groups engaged in medical diagnosis. Although the major players are domestic companies, many of them received significant amounts of foreign investments, as discussed above. Also, it is worth noting that although these companies have a core business, a significant degree of diversification is taking place in the segment, with medical diagnosis companies having acquired hospitals and hospital chains offering diagnostic services.

The next two charts present information on the ten largest companies in Brazil in the pharmaceuticals and health services segments.

An important aspect related to major players in the healthcare sector in Brazil is the intense activity of mergers and acquisitions taken place in recent years. This activity involved mainly operations between hospitals/clinics chains and health insurance providers.

Examples of major mergers and acquisitions transactions in the sector include the acquisition of health insurance provider SulAmérica by hospital chain Rede D’Or and the merger between health insurance providers Hapvida and NotreDame Intermédica. Before the merger, both Hapvida and NotreDame Intermédica had been involved in acquisitions of health insurance providers and hospitals and clinics. The intense level of activity is explained by the high volume of cash held by major players after they initially floated their shares (Hapvida and NotreDame Intermédica in 2018 and Rede D'Or in 2020).

In addition, companies specialised in diagnostic medicine have also been involved in recent consolidation processes. In April 2023, Brazil’s antitrust body approved the merger between Fleury and Hermes Pardini, second and third largest companies in the segment, respectively.

It is also worth noting the interest of private equity funds in the healthcare sector. For instance, Patria Investimentos, a major fund in Brazil, established a group called Athena, which owns hospitals, clinics and health insurance operators.

CONCLUSION AND SUMMARY OF OPPORTUNITIES

Brazil’s healthcare sector is one of the largest in the world, and the country presents plenty of opportunities for Finnish companies willing to access the market. Important aspects affecting the profile of the market is the profound demographic transition Brazil is currently experiencing, with elderly people accounting for an increasing share of the country’s population, and the high degree of urbanisation influencing major causes of death. Companies offering products and solutions directed at the care of elderly people and engaged in the treatment and prevention of causes affecting highly urbanised societies will certainly find in Brazil a relevant market to explore.

Another important aspect to be considered is the increasing degree of digitalisation in the sector that is currently taking place in Brazil, and the fact that recently important pieces of legislation were put in place to regulate the use of technology in healthcare in Brazil. Regarding digitalisation, it is also worth noting the ambitious government strategy to deepen the adoption of information technology in healthcare in Brazil. Considering these recent developments, Brazil is also a relevant market for Finnish companies engaged in offering technology-based solutions in the healthcare sector, including health technology start-ups.

It is also important to consider the fact that both the public and private sectors are massive players in the Brazilian healthcare industry and the two blocs demand huge volumes of goods and services. In terms of products purchased from abroad, Brazil is a larger importer of pharmaceuticals, and generics have a significant share of medicines sales in the country. Imports of medical supplies and equipment are also sizeable, and considering the main characteristics of the Finnish economy this could also be an important target of healthcare companies from Finland.

Finally, another important aspect of the Brazilian healthcare market is the fact that, in addition to large domestic companies, foreign enterprises also occupy leading positions in the industry, particularly in the pharmaceuticals segment. And recently an intense activity of mergers and acquisitions led to greater concentration of the market and an increasing level of diversification for important players, especially in health services and health insurance.

Text: Rafael Murgi, Coordinator, Commercial Affairs, Consulate of Finland, São Paulo.

REFERENCES

Ministry of Health. (2012). Portaria nº 837, de 18 de abril de 2012. Define as diretrizes e os critérios para o estabelecimento das Parcerias para o Desenvolvimento Produtivo (PDP). Retrieved April 5, 2023

Ministry of Health. (n.d.). Parcerias para o Desenvolvimento Produtivo. Retrieved April 5, 2023.

Ministry of Health. (n.d.). Rede Nacional de Dados em Saúde - RNDS. Retrieved April 5, 2023

Brazilian Health Regulatory Agency. (2022). RDC nº 657, de 24 de março de 2022. Dispõe sobre a regularização de software como dispositivo médico (Software as a Medical Device - SaMD). Retrieved April 5, 2023

Brazilian Health Regulatory Agency. (2022). Resolução - RDC nº 741, de 10 de agosto de 2022. Dispõe sobre os critérios gerais para a admissibilidade de análise realizada por Autoridade Reguladora Estrangeira Equivalente em processo de vigilância sanitária junto à Anvisa. Retrieved April 11, 2023

Collucci, C. (2019, April 29). Saída de fábricas do Brasil preocupa setor farmacêutico. Folha de S. Paulo. Retrieved April 13, 2023

Columbia University Mailman School of Public Health. (n.d.). BRAZIL | Summary. Retrieved April 17, 2023

Euclydes, C. (2023, February 2). Fusões e aquisições no setor de saúde devem crescer este ano, com foco regional, diz consultoria. Valor Econômico. Retrieved April 13, 2023

Federal Senate of Brazil. (2015). Lei nº 13.097, de 19 de janeiro de 2015. Retrieved April 11, 2023

Forbes. (2019, December 18). Hypera compra Buscopan e outros ativos da Boehringer por R$ 1,3 bilhão. Forbes. Retrieved April 13, 2023

Forbes. (2020, March 2). Hypera compra portfólio de medicamentos da Takeda por US$ 825 milhões. Forbes. Retrieved April 13, 2023

G1. (2015, September 16). Advent compra 13% do capital do Fleury e prevê novas aquisições. Retrieved April 17, 2023

Guimarães, F. (2022, March 14). Onda de fusões na saúde movimenta R$ 20 bi em um ano e aquece o setor. O Estado de S. Paulo. Retrieved April 13, 2023

International Trade Administration. (2023, March 28). Brazil - Country Commercial Guide. Retrieved April 17, 2023

Koike, B. (2017, September 21). Advent capta R$ 1,3 bi com Fleury. Valor Econômico. Retrieved April 17, 2023

Koike, B. (2019, December 20). Setor de saúde bate recorde em fusões e aquisições neste ano. Valor Econômico. Retrieved April 13, 2023

Koike, B. (2022, December 30). Com juro alto, saúde troca aquisições por fusões em 2022. Valor Econômico. Retrieved April 13, 2023

Lucchesi, C. (2021, June 17). Goldman quer vender fatia na Oncoclínicas após ganho de 8 vezes. Bloomberg. Retrieved April 17, 2023

Ministry of Health. (2020). Brazilian National Digital Health Strategy 2020-2028. Retrieved April 5, 2023

Ministry of Health. (2020). Portaria nº 1434, de 28 de maio de 2020. Institui o Programa Conecte SUS e altera a Portaria de Consolidação nº 1/GM/MS, de 28 de setembro de 2017, para instituir a Rede Nacional de Dados em Saúde e dispor sobre a adoção de padrões de interoperabilidade. Retrieved April 5, 2023

Olivon, B. (2023, April 12). Tribunal do Cade aprova fusão entre Fleury e Hermes Pardini. Valor Econômico. Retrieved April 13, 2023

Organisation for Economic Co-operation and Development. (2021). OECD Reviews of Health Systems: Brazil 2021. (O. Publishing, Ed.) doi

Organisation for Economic Co-operation and Development and The World Bank. (2020, June 16). Health at a Glance: Latin America and the Caribbean 2020. doi

Presidency of the Federative Republic of Brazil. (1990). Lei nº 8.080, de 19 de setembro de 1990. Dispõe sobre as condições para a promoção, proteção e recuperação da saúde, a organização e o funcionamento dos serviços correspondentes e dá outras providências. Retrieved April 17, 2023

Presidency of the Federative Republic of Brazil. (2017). Decreto nº 9.245, de 20 de dezembro de 2017. Institui a Política Nacional de Inovação Tecnológica na Saúde. Retrieved April 5, 2023

Presidency of the Federative Republic of Brazil. (2022). Lei nº 14510, de 27 de setembro de 2022. Altera a Lei nº 8.080, de 19 de setembro de 1990, para autorizar e disciplinar a prática da telessaúde em todo o território nacional, e a Lei nº 13.146, de 6 de julho de 2015. Retrieved April 5, 2023

PwC. (2013). The Healthcare market in Brazil. Retrieved April 17, 2023

Scheffer, M., & Senra Souza, P. M. (2022). A entrada do capital estrangeiro no sistema de saúde no Brasil. Cad. Saúde Pública, 2. doi

Tagatiba, M., & de Paula, L. (2023, April 10). Regulamentação da telemedicina impacta a formação médica e expõe desafios que ultrapassam a tecnologia. Saúde Business. Retrieved April 11, 2023

Tooge, R. (2023, February 20). Após acelerar consolidação, setor de saúde deve ‘digerir’ aquisições em 2023. InfoMoney. Retrieved April 13, 2023, from