Business opportunities in the mining sector in Brazil

KEY TAKEAWAYS

- Brazil is a prominent player in the global mining sector. The country is one of the largest mineral producers in the world and hosts relevant reserves of various strategic substances.

- Iron ore stands as the primary product of Brazil's mining sector and the country produces significant volumes of gold, copper, nickel, bauxite (aluminium) and manganese.

- The global energy transition represents a relevant opportunity for the mining sector in Brazil, as the country is rich in the critical resources required for the transition to a low-carbon economy.

- Due to its relevance in the sector, Brazil is an attractive destination for businesses offering solutions in a wide range of segments that support mining activities.

- Finnish companies may find in the country plenty of opportunities in areas including environmental solutions, circularity, net-zero mining, safety, logistics and digitalisation and intelligent mining.

INTRODUCTION

This report intends to provide useful information and analysis for Finnish companies interested in accessing the Brazilian mining sector. This study will cover aspects related to the production of metallic and non-metallic ores, excluding substances such as oil, gas and coal.

The first section of the report will briefly present information on the Brazilian regulatory framework for the mining sector, highlighting especially the role of the main government organisations involved in the industry. The following section will provide information that shows the international relevance of Brazil in the mining sector both in terms of output and exports. Next, the report will present information on the most important minerals for Brazil, considering the production and reserves of minerals. The following two sections will analyse trends in Brazilian mining, taking into account production, exports and investments. Before discussing the relations between Brazil and Finland in the sector, the report will analyse the regional profile of mining in Brazil and provide information on the main players in the sector. Lastly, the study will present the main conclusions and a summary of opportunities.

Brazil is a prominent player in the global mining sector. The country is one of the largest mineral producers in the world and hosts relevant reserves of various strategic substances. With a significant portion of its territory yet to be geologically mapped, Brazil holds considerable opportunities in terms of expansion in mining activities and increase of exports.

Brazil produces significant volumes of important mineral substances including gold, copper, nickel, bauxite (aluminium) and manganese. The country is the largest producer of niobium globally. Iron ore stands as the primary product of the country's mining sector, and Brazil is the second-largest producer of iron in the world, accounting for nearly 20% of the market. Also, iron ore constitutes the majority of the country’s exports in the mining sector. Vale, a company headquartered in Rio de Janeiro that was privatised in 1997, stands as the world's largest iron ore producer and the third-largest mining company overall.

The global energy transition represents a relevant opportunity for the mining sector in Brazil, as the country is rich in the critical resources required for the transition to a low-carbon economy. Moreover, the federal government inaugurated in January 2023 considers decarbonisation a priority for Brazil. These aspects signal that the mining industry in the country can take a leading role in sustainability issues, not only by providing the mineral products necessary for global decarbonisation efforts but also by contributing to the reduction of deforestation and engaging in reforestation initiatives, particularly in the Amazon region.

BRIEF DESCRIPTION OF THE REGULATORY FRAMEWORK

Mining in Brazil is subject to federal regulation, and the Mining Code (Decree Law No. 227/1967) establishes the fundamental framework for industry regulation. Numerous federal institutions oversee the mining sector, including the Ministry of Mines and Energy (MME), the National Mining Agency (ANM) and the Geological Service of Brazil (CPRM). Additionally, other governmental bodies regulate labour, environmental and safety aspects of the industry. As regards environmental matters, in many cases subnational regulations may apply.

Established in 2017 to modernise regulatory frameworks, the National Mining Agency (ANM) replaced the National Department of Mineral Production. The duties of the ANM include enforcing mining regulations, promoting the management of the country’s mineral resources and issuing mining rights. Its creation is considered a significant improvement in regulatory efficiency and transparency, inasmuch as the organisation has been offering clearer guidelines and more transparent management of mining titles.

The National Mineral Policy Council (CNPM) functions as the coordinating body for public policies aimed at developing Brazil's mineral sector. Its responsibilities include formulating sustainable policies for various segments in the mineral industry, including dam safety and the integration of mining within the national strategy for energy transition. Recently, the CNPM was restructured to enhance its advisory role to the government regarding the formulation of policies and the provision of guidelines for the development of the Brazilian mining industry.

INTERNATIONA RELEVANCE OF BRAZIL IN THE MINING SECTOR

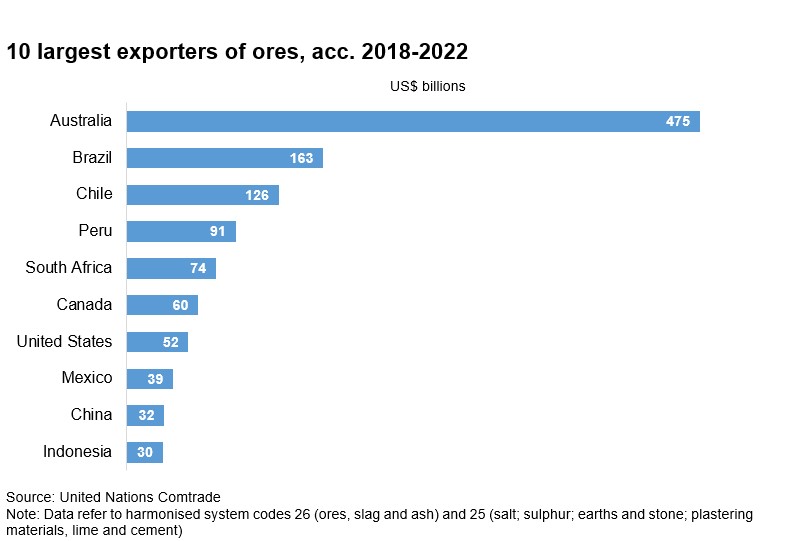

Brazil is one of the most significant players in the mining sector in the world, both in terms of production and exports. In regard to the production value of mineral ores, estimates indicate that Brazil is the third largest market globally, following China and Australia. In relation to exports, the country is the world’s second largest exporter of minerals, trailing behind Australia. The size and relevance of Brazil’s mining industry create a myriad of opportunities for companies providing goods and services along the mineral extraction value chain. The following two charts provide information on the production and export volumes for the most important countries in the mining sector.

MAIN MINERALS PRODUCED IN BRAZIL

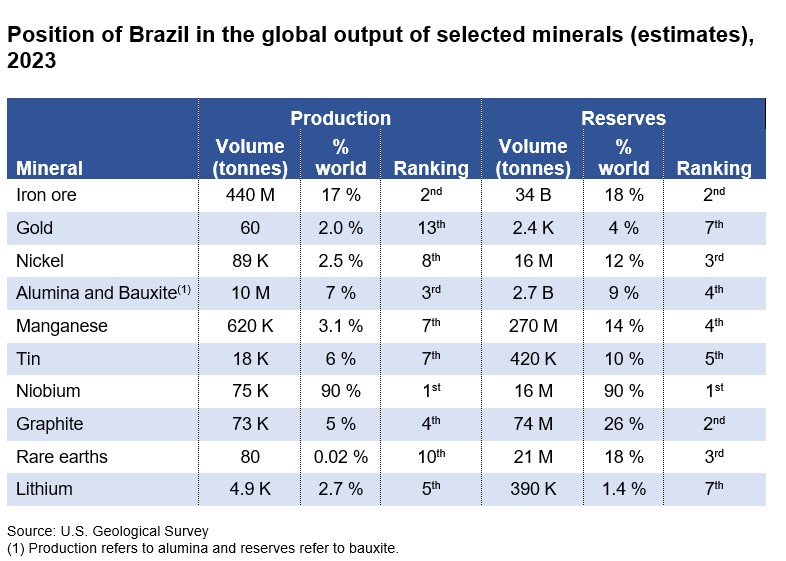

Brazil possesses significant geological potential due to its vast land area and abundant reserves of key metals. The three primary mineral commodities in Brazil in terms of economic value are iron ore, copper and gold. The country ranks in the first positions in terms of reserves of important minerals such as nickel, manganese, bauxite and tin, and it stands as the largest producer of niobium globally. Moreover, Brazil hosts substantial reserves of strategic minerals for energy transition, including graphite, lithium and rare earth elements.

It is worth noting that for a group of critical minerals that include nickel, manganese graphite and rare earths, there are significant differences between the worldwide share of reserves hosted by Brazil (ranging between 12% and 26%) and the country’s share of global production (ranging between 0.02% and 5%). That indicates that for these minerals production levels are below their potential and it reinforces the need for investments in the mining sector in Brazil.

The following table shows information about Brazil’s worldwide share in the production and reserves of selected minerals.

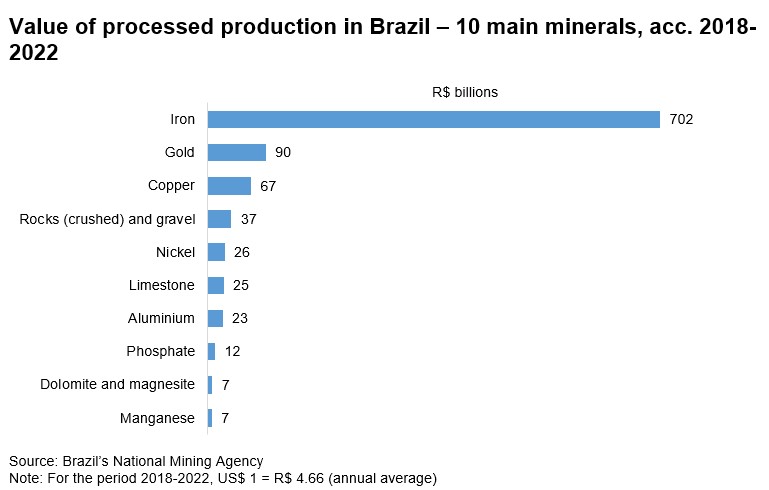

The value of mineral production in Brazil is highly concentrated in iron ore, gold and copper. Iron is by far the most important substance produced by the mining industry in Brazil. Between 2018 and 2022, iron ore accounted for 67% of the production value in the sector. Gold and copper are the second and third most important minerals, with production value shares between 2018 and 2022 of 9% and 6%, respectively. For this period, the three main metals produced in Brazil accounted for 82% of production value. Iron ore, gold and copper are followed by rocks and gravel, nickel, limestone and aluminium, with significantly smaller production values. The following chart shows information on the main mineral substances produced in Brazil.

TRENDS IN PRODUCTION AND EXPORTS OF MINERALS

In the last decades, the production and exports of Brazilian minerals have been following an overall upward trend. Between 2003 and 2011, influenced by the commodities boom of the early 21st century, the value of mineral production and exports rose sharply. Next, from 2012 to 2016, the variables followed a downward trend due to the end of the commodities boom that resulted in lower metal prices. In this period, output was also negatively affected by the suspension of some iron ore operations following the Mariana dam disaster in 2015. From 2017, there has been a new rise in mineral output and exports as a consequence of a recovery in commodity prices. The next two charts show the trajectories of the production and exports of Brazilian minerals since the second half of the 1990s.

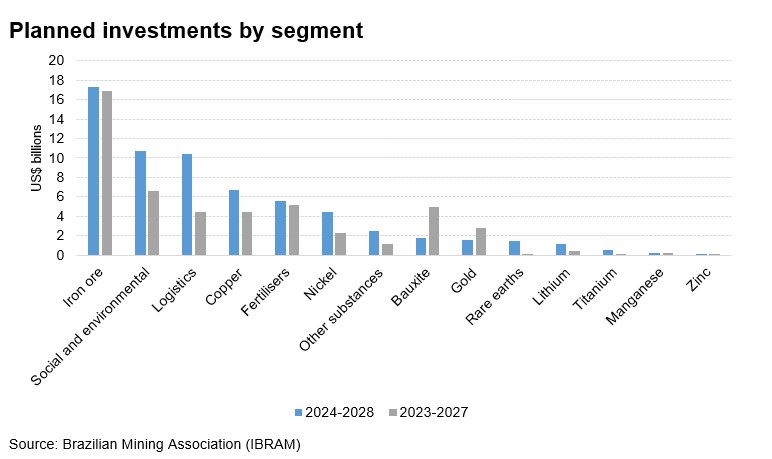

In addition to influencing the output and exports of minerals, the worldwide demand for minerals and their prices in the international markets also impact the planned investments of companies operating in the mining sector in Brazil. During the commodities boom of the early 21st century, planned investments reached record highs, with a peak in 2012. Since 2017, a new upward trend has been taking place, albeit with lower levels in relation to the first years of the 2000s. As seen in the chart below, for 2024 the 5-year investment plans from the companies operating in the mining sector in Brazil total US$ 65 billion, a sign that companies are foreseeing intense activity in the next years, even in a scenario of uncertainty at international level.

For the next years, projects to extract iron ore, copper and nickel are expected to receive significant amounts of investments. Also, due to the relevance that the agribusiness sector plays in the Brazilian economy and the high dependence of the country on imports of fertilisers, high investment volumes in new potassium mines are planned. Other substances that are associated with large volumes of planned investments are bauxite, gold, rare earth elements and lithium. Social and environmental issues are expected to be the second largest segment in terms of investments in the next five years. These expenditures have been highly influenced by two major tragedies taken place recently in Brazil, the dam disasters of Mariana in 2015 and of Brumadinho in 2019. The following chart presents information on the planned investments in Brazil by segment.

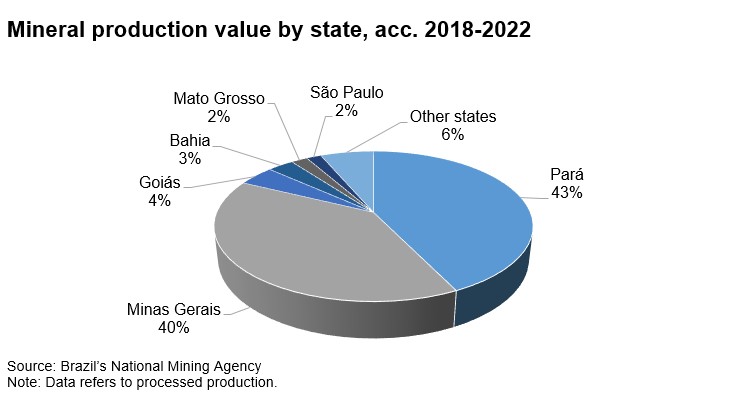

Mining activity in Brazil is highly concentrated on the states of Pará and Minas Gerais. These states account for more than 80% of mineral production value in the country. Other states in Brazil hosting relevant activities in mining include Goiás, Bahia, Mato Grosso and São Paulo. Information about the regional activity in the mining sector in Brazil are shown in the chart and map below.

In terms of the main substances produced in each state, Pará has been a significant producer of iron ore, copper and bauxite. In fact, the state of Pará hosts the largest iron mine in the world, the Greater Carajás Project. In Minas Gerais, production of iron ore and gold prevails, and the state presents great potential in critical minerals such as lithium and rare earth elements.

The state of Goiás has a significantly diversified mineral production, with nickel, copper, gold, niobium, phosphate and limestone as the main substances. In Bahia, gold and copper are the main metals produced, and in Mato Grosso the production of gold is the most relevant. In the state of São Paulo, Brazil’s largest state in terms of economy and population, mineral activity is primarily associated with the extraction of minerals used in the construction industry, with a predominance of rocks and gravel.

Mineral extraction in Brazil is carried out by Brazilian conglomerates and subsidiaries of large multinational companies, with a big share of revenues generated by Vale, one of the largest mining companies in the world. Following the distribution of mineral resources in the country, the main companies operating in the mining sector in Brazil are not headquartered in São Paulo, in contrast to most sectors of the Brazilian economy.

In the mining sector, there is a high degree of complementarity between Finland and Brazil, with a good number of Finnish companies providing information and communications technology solutions and machinery and equipment to the main mining companies in the country. Examples Finnish players engaged in the mining sector in Brazil include AFRY, Metso, Normet, Sandvik in engineering and machinery and Nokia in private communication networks.

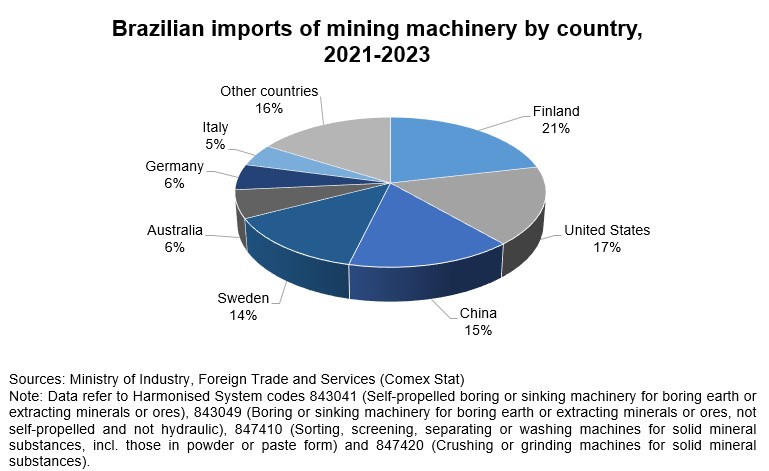

Finnish companies are particularly relevant suppliers of mining equipment to Brazil. It is worth mentioning that the Brazilian market for mining equipment is highly competitive, and several multinational companies in the sector have production units in the country, from where they serve the domestic market and frequently export to other countries. For companies without a local subsidiary, it is advisable to collaborate with a Brazilian representative capable of offering technical and support services and managing import procedures.

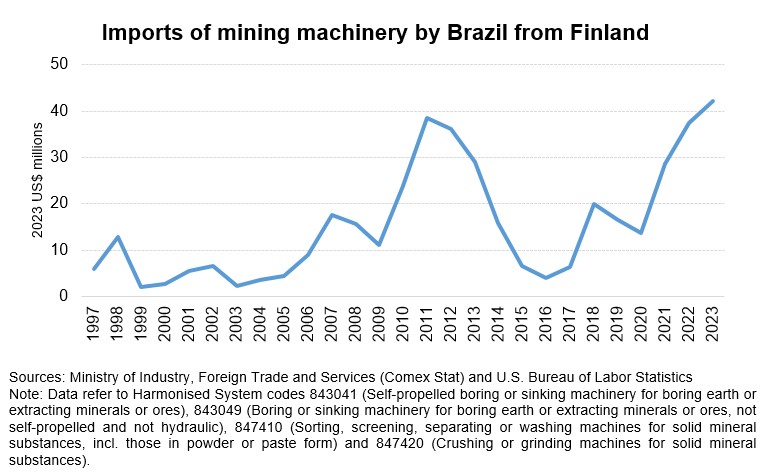

In the last decades, the trajectory of imports of mining machinery by Brazil from Finland has shown a similar pattern in relation to output and exports, with a sharp rise during the 2000s commodities boom followed by low values in the mid-2010s and a recovery from 2017. For mining machinery (Harmonised System codes 843041, 843049, 847410 and 847420), import taxes applied by Brazil may be relatively high, with rates that can be 9% or 12.6%, while some products are exempt from import taxes. It is worth noting that mining equipment is also manufactured locally by Finnish companies.

CONCLUSION AND SUMMARY OF OPPORTUNITIES

Brazil has significant mineral resources in its vast territory and mining is one of the main sectors of the Brazilian economy. Brazil is one of the major players in the global mining industry, and due to its relevance in the sector the country is an attractive destination for businesses offering solutions in a wide range of segments that support mining activities.

Currently, the reduction of environmental impacts generated by mining is one of the major challenges facing the sector, and this agenda is of great significance for companies operating in Brazil. From extraction, through beneficiation, to waste disposal, environmental issues are present in various stages of mining. It is worth noting that mining is part of the supply chain for various industrial products, which renders the activity subject to significant social scrutiny. There are widespread expectations that the sector moves towards decarbonisation and that key players act in accordance with other goals related to environmental, social and governance (ESG) aspects.

Investments to promote more efficient use of natural resources and to adopt circular production methods have been an important current focus in the sector's efforts towards sustainability. Mining often requires significant consumption of water and electricity, and a key objective of the sector is improving efficiency in the use of these natural resources. Efforts are also directed towards promoting greater use of recycled materials and improving waste management, including the reuse of tailings.

The growing demand for minerals and metals produced in a cleaner and more sustainable manner also presents new opportunities for the mining sector in Brazil. The country is a global leader in clean energy generation capacity, particularly in electricity, whose share of production originating from renewable sources stands at over 80%. Given its significant capacity to generate energy from renewable sources and the recent expansion of investments in solar and wind power in the country, Brazil has strong potential to become a global leader in net-zero mining.

Efforts directed towards increasing the safety of mineral extraction operations represent another highly relevant trend in the sector in Brazil. Two major disasters involving the collapse of dams occurred in the country in recent years, and operational safety is currently a major concern for mining companies operating in Brazil. This trend presents an opportunity for suppliers that can provide the solutions needed to mitigate the risks associated with mining extraction in the country.

Brazil also offers several opportunities that derive from the size of its territory and the geographical profile of mining activities. Brazil has a vast territory and most of the mining activity in the country takes place in areas that sorely need infrastructure investments. This results in opportunities for companies involved in many aspects related to transport and logistics, particularly the construction, improvement and maintenance of railways and roads. It is worth noting that some of the major mining areas in Brazil coincide with the Amazon region, which makes mining in Brazil challenging not only in terms of logistics but also when it comes to issues involving sustainability.

The mining sector in Brazil also presents vast opportunities for information and communications technology companies and firms offering solutions in intelligent mining. The sector has been increasingly utilising advanced technologies in its activities and it has been investing to automate various stages of operations through tools such as autonomous machines, big data, artificial intelligence and the Internet of Things (IoT). For companies in the sector, there is also significant potential related to mapping, as Brazil has a considerably low level of territory mapping compared to other countries in which the mining sector has a key role, such as Australia and Chile.

In sum, the mining industry in Brazil is a good example of a sector in which there is a high level of economic complementarity between Brazil and Finland. The sector presents a myriad of opportunities for Finnish companies willing to access the Brazilian market. In addition to the provision of high-technology inputs, Finnish companies may find in the country plenty of opportunities in areas including environmental solutions, circularity, net-zero mining, safety, logistics and digitalisation and intelligent mining.

At last, it worth mentioning that every year Brazil's mining association organises one of the most relevant mining events in Latin America, the Brazilian Mining Congress (EXPOSIBRAM). The event gathers the most important companies in the world of the mining and metals sector and hosts renowned sector specialists to discuss trends in the domestic and global markets. The congress represents an excellent opportunity for Finnish companies willing to interact with relevant entities involved in the sector including mining companies, suppliers, government organisations and trade associations. This year’s edition of the event will be held from 9th to 12th September at the Expominas Exhibition Centre in Belo Horizonte.

For additional information on the sector and support in the Brazilian market, please contact Matti Landin (matti.landin@businessfinland.fi) and Rafael Murgi (rafael.murgi@gov.fi).

Text: Rafael Murgi (PhD), Coordinator, Trade and Economic Affairs at the Consulate of Finland in Sao Paulo.

The full version of the report, including graphs, is available at finlandabroad.

REFERENCES

Alves, F. (2023). Brazil is more than just iron ore. Brazil Mineral (Special Issue). Retrieved March 1, 2024

Alves, F. (2023). New projects herald return to growth for Brazil's mining industry. Brazil Mineral (Special Issue). Retrieved March 1, 2024

Bernal, A., Husar, J., & Bracht, J. (2023, April 2023). Latin America’s opportunity in critical minerals for the clean energy transition. Retrieved March 1, 2024, from International Energy Agency.

Deloitte. (n.d.). O papel indispensável da mineração e dos metais: Estudo global da Deloitte destaca 10 tendências para o setor nos próximos meses. Retrieved March 1, 2024, from As Tendências de Mineração 2023.

Guyon, M., Preciado, N., Flaherty, M., & Turk, A. (2023). Brazil Mining. Global Business Reports. Retrieved March 1, 2024

International Trade Administration. (2022, June 6). Brazil Mining Sector. Retrieved March 1, 2024, from Market Intelligence.

Metso. (2020, May 20). Indústria de mineração no Brasil e seu crescimento. Retrieved February 19, 2024

Ministry for Foreign Affairs of Finland. (2022). Mining Sector in Brazil. Retrieved February 15, 2024

Moraal, W. (2018). Sectorschets Mining NBSO Brazil. Belo Horizonte. Retrieved March 1, 2024

Nanô, F. L. (2023). Overview of Brazil's infrastructure sectors and opportunities. Swiss Business Hub Brazil. Retrieved February 15, 2023

OECD. (2022). Regulatory Governance in the Mining Sector in Brazil. Paris: OECD Publishing.

Oliveira, B. (2015). Relatório de benchmark - mineradora do futuro 2030. Fundação Dom Cabral. Retrieved February 15, 2024

Sartorio, A., Balbi, B., & Brito, J. (2023). Riscos e Oportunidades de Negócios em Mineração e Metais no Brasil em 2023. EY; IBRAM. Retrieved February 16, 2024

Secretaria de Comunicação Social. (2023, April 9). Conselho Nacional de Política Mineral é restruturado. Retrieved March 6, 2024